In Hong Kong, crypto-trader Sam Bankman-Fried stole naps on his office beanbag to get through 18-hour days as demand surged for digital assets. At an auction in Wellington, Darryl Harper pronounced the New Zealand housing market “ferocious” as he brought the hammer down on homes going for hundreds of thousands of dollars above their official valuations. In Makati City, the Philippines, AC Energy Corp. Chief Financial Officer and Treasurer Corazon Dizon was overwhelmed by the appetite for a $300 million green bond. And in Midtown Manhattan, hedge fund manager David Einhorn marveled over a job application from a 13-year-old who claimed he’d quadrupled his money.

A common thread runs through these scenes from the plague year 2020: Cheap money, gushing in from the world’s major central banks, inflated assets and reshaped how we save, invest, and spend. And that’s not the end of it. Unlike past recoveries, when investors had no clarity on when the monetary taps would be tightened, this time officials have explicitly said they’re going to stick to their loose policies well into a post-Covid recovery.

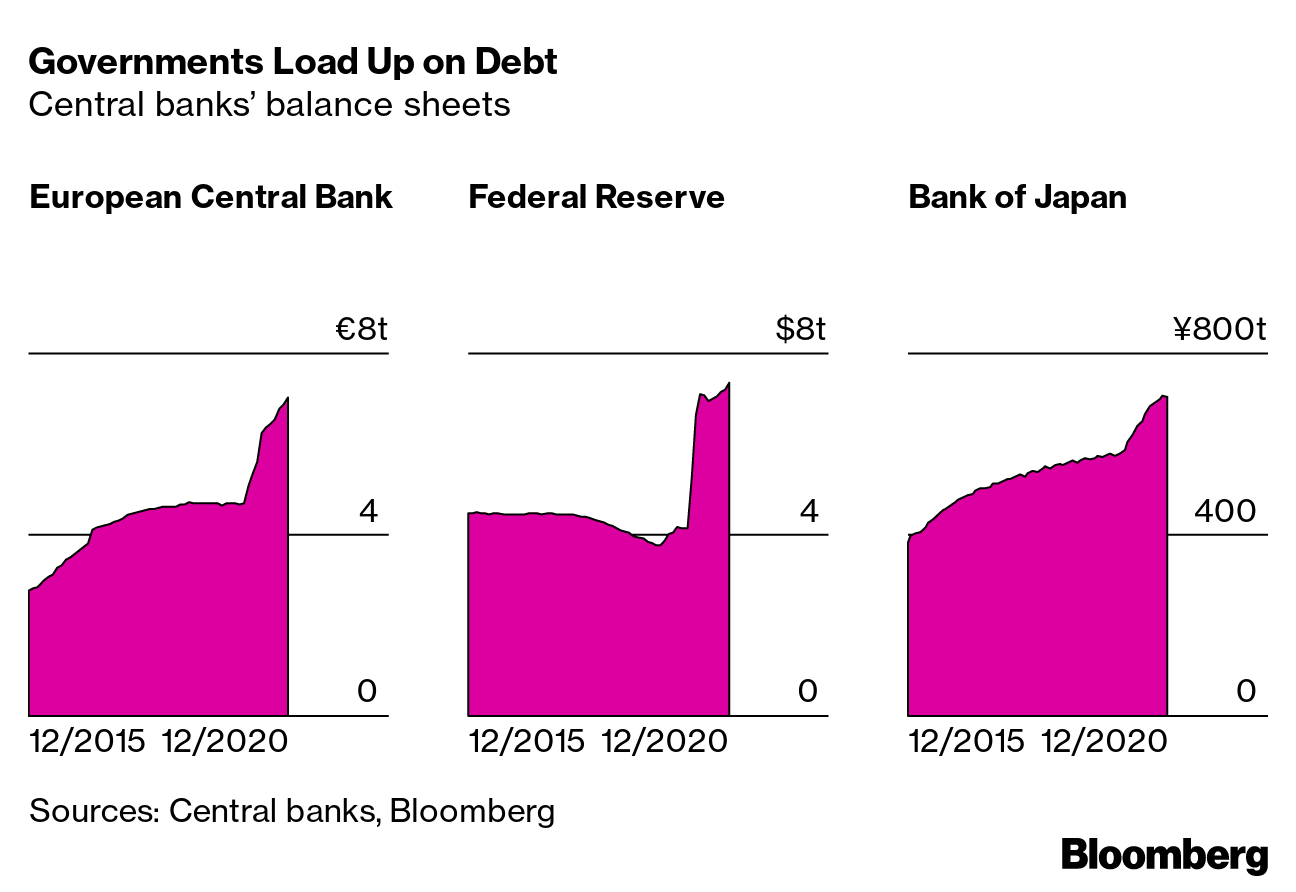

Governments Load Up on Debt

Central banks’ balance sheets

The strategy is clear and deliberate: Snuff out volatility from the bond market and make debt the cheapest it’s ever been to deter saving and encourage investment. The hope: Cheap cash leads companies to invest and hire as rising asset prices make people more confident and ready to spend. The inevitable side effect: More volatility for assets (apart from bonds) as investors chase returns around the world. And, of course, the risk: Bloated asset prices pop, undermining financial stability before the real economy can benefit from all that cash.

“There is no escaping that if you enhance liquidity dramatically, the money will go in search for yield and certainly can expose assets to mispricing,” says Agustín Carstens, general manager of the Basel, Switzerland-based Bank for International Settlements, the so-called bank for central banks. “This is a risk and something that needs to be recognized and that needs to be watched very, very carefully.”

Signs of bubbles are everywhere as stock prices jumped by a magnitude not seen since the dot-com era, new share listings boom, and Bitcoin, though volatile, continues its generally upward climb. But if company earnings fall short of expectations or the vaccine rollout falters, there’s a risk markets will lurch as investors take money off the table.

Central bankers, from the U.S. Federal Reserve’s Jerome Powell on down, are well aware of the danger. Surging valuations—some investors call what’s happening “the everything rally”—have been too obvious to ignore. Powell, Bank of Japan Governor Haruhiko Kuroda, and other leading central bankers, though taken to task about bubbles in markets in recent months, have played down the concerns. That’s in part because they’re mindful of the danger of closing the monetary spigot too quickly. Indeed, coming out of the last crisis a decade ago, policymakers in some economies were probably too quick to withdraw stimulus for fear of creating bubbles and ended up putting the brakes on the economic recovery.

When the pandemic’s spread led to shutdowns across much of the world, most central banks went all in. They slashed positive interest rates to near zero; where rates were already razor-thin, they massively increased asset purchases; many set up emergency funding for struggling companies; and this time most pledged to keep their unprecedented settings for the next few years. Across 2020, governments rolled out at least $12 trillion in fiscal stimulus, according to the International Monetary Fund, and central banks provided trillions more in monetary support.

It worked. Global bond markets that showed alarming signs of dislocation last March turned calm. Stock markets rallied. Currencies in emerging markets strengthened, letting their central banks get in on the easing act, too. The result has been extraordinarily low yields even for the longest-dated debt securities and traditionally riskier borrowers.

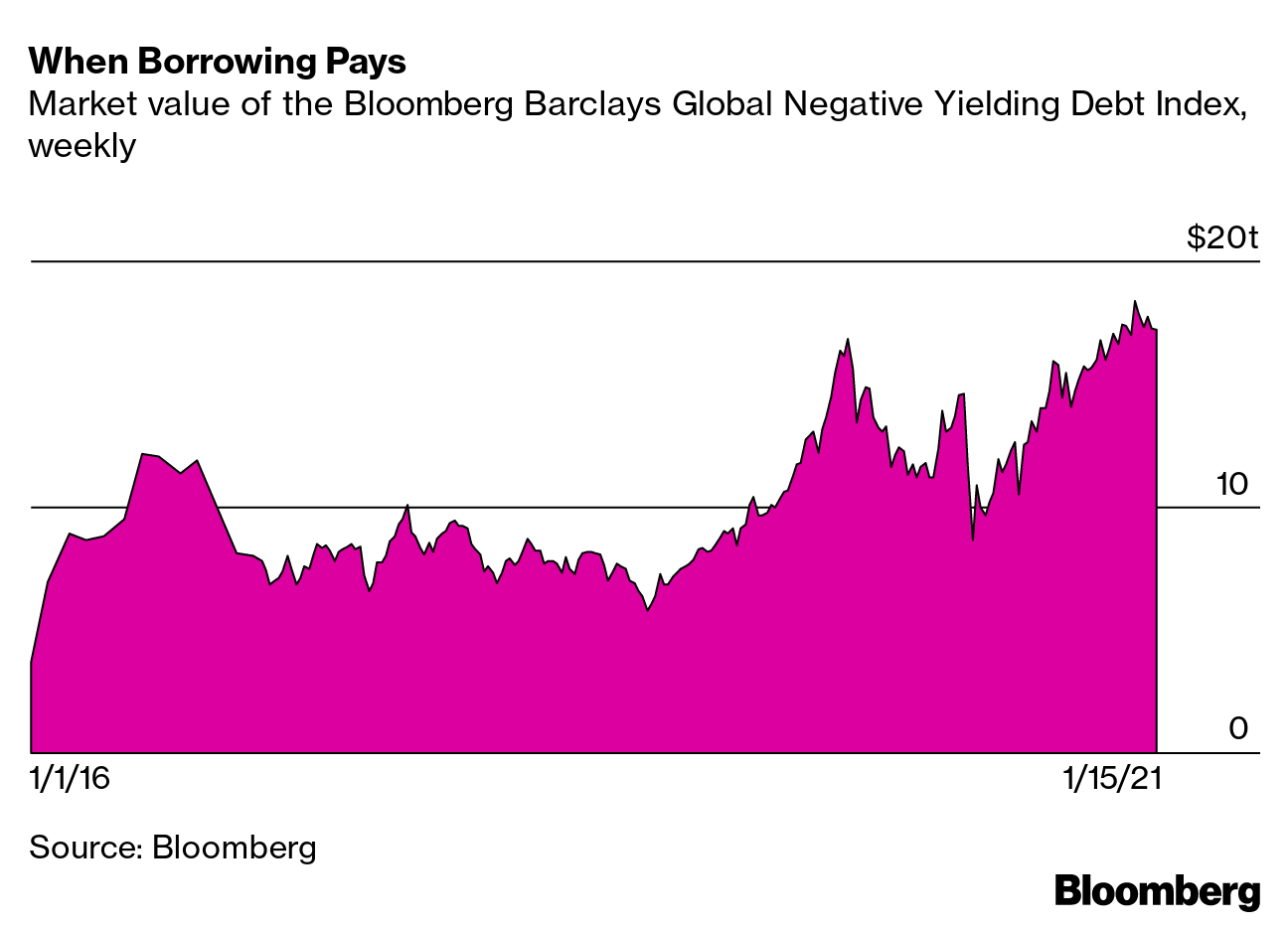

As of Dec. 31, $17.8 trillion in debt was trading with a negative yield. Governments from Australia to Spain were effectively getting paid to borrow. Junk bonds in the U.S. were trading at yields similar to those of investment-grade corporate debt that priced just two years earlier. When Peru sold a debut 100-year bond in November, the instrument became the lowest-yielding security of such maturity ever issued by the government of a developing economy.

“Central banks, and especially the Fed, have already created bubbles,” says Alicia García-Herrero, chief Asia-Pacific economist at Natixis SA in Hong Kong, who previously worked for the IMF and the European Central Bank. She points to the disconnect between booming markets and a very uneven economic recovery. “Central banks know what they are doing—basically lowering the return of safe assets to increase demand for risky ones. Once you do that, you know a bubble might appear, but the cost of not doing anything is probably even higher.”

When Borrowing Pays

Market value of the Bloomberg Barclays Global Negative Yielding Debt Index, weekly

When the auction of seven houses met with frenetic bidding in Wellington in November, a modest 80-square-meter, three-bedroom cottage went for NZ$945,000 ($678,000)—well above the so-called rateable valuation of NZ$640,000 assessed by the local government. “Interest rates historically have never been lower,” says Harper, the auctioneer. “So it’s easy for buyers to borrow.”

While New Zealand’s central bank had managed to skirt the global financial crisis without resorting to quantitative easing, the pandemic blew that up. The Reserve Bank of New Zealand cut interest rates and launched a bond-buying program—the impact of which, coupled with a supply shortage, lit up the nation’s house prices. With rock-bottom borrowing costs stoking demand for homes, the government took the unusual step of asking the RBNZ to take the housing market into account when it sets its policies—a move the bank resisted.

Bidding for their first home, Harriette McClelland and Harry Greenwood, both in their late 20s, missed out when the price approached NZ$1.2 million. “I’m disappointed,” McClelland said at the time. She pinned some of the blame on a lack of supply, adding, “but obviously low interest rates have really escalated things a lot.”

That disappointment is mirrored globally as inequality deepens across different population groups. Owners of appreciating assets are enjoying hearty gains in wealth, while those without them are missing out.

The world’s 500 richest people added $1.8 trillion to their combined net worth last year, taking it to $7.6 trillion, according to the Bloomberg Billionaires Index. Until January, Amazon.com Inc. founder Jeff Bezos remained the world’s richest person, thanks to surging enthusiasm for online retail during lockdown. Then, in possibly the fastest bout of wealth creation in history, Elon Musk leapt into first place after Tesla Inc. skyrocketed in value. Combined, these two men gained about $217 billion in 12 months, enough to send $2,000 checks to more than 100 million Americans.

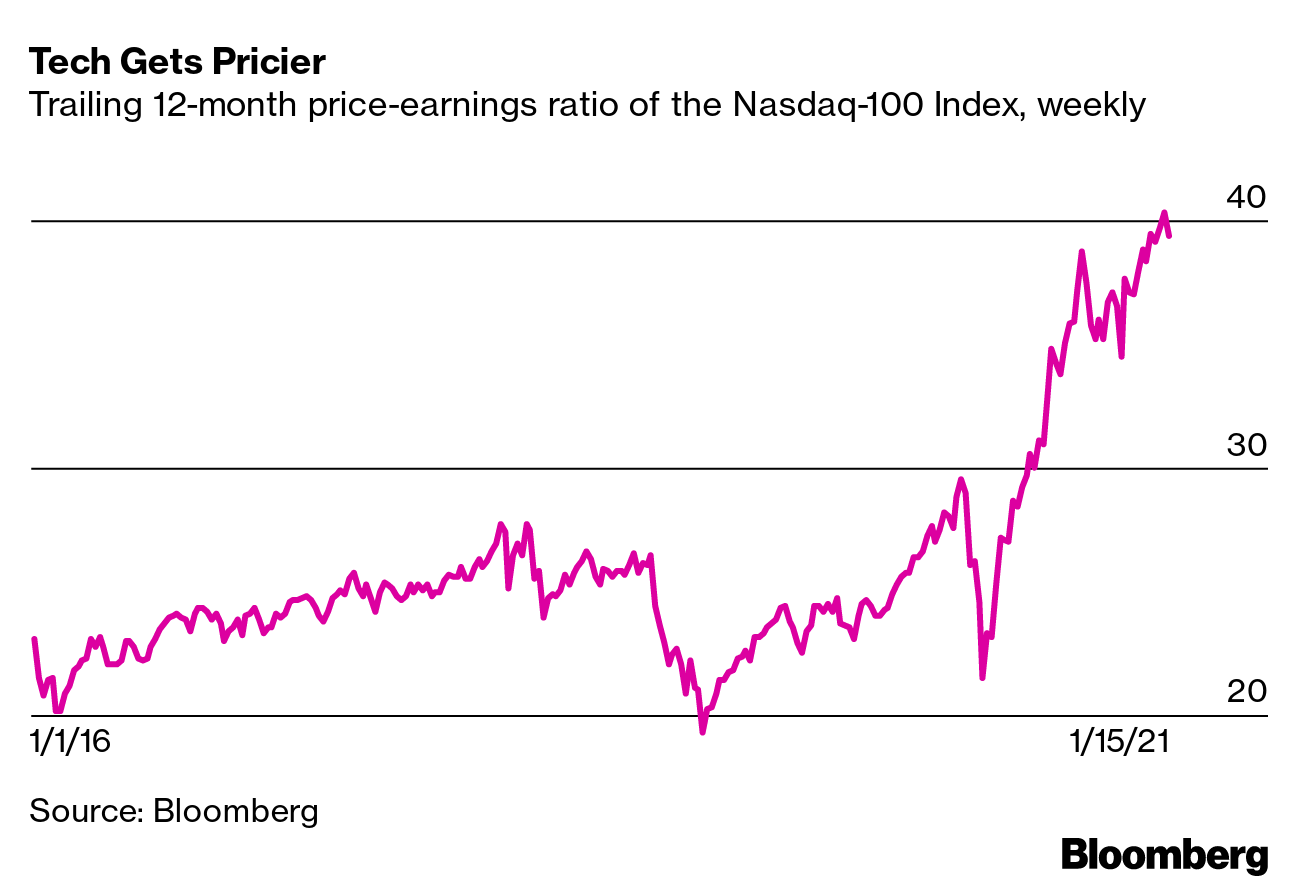

Tech Gets Pricier

Trailing 12-month price-earnings ratio of the Nasdaq-100 Index, weekly

Critics say central bankers are deepening inequality by whipping markets to frothy heights while doing little for wage gains or job creation in the real economy. On the other hand, there’s the argument that in the end, monetary policy is limited in what it can do to heal a shattered economy. Reserve Bank of Australia Governor Philip Lowe acknowledged as much in testimony to lawmakers in Canberra in December: “All I can do is try to make the aggregate strong,” he said.

What’s needed instead is more government spending, according to the likes of former U.S. Treasury Secretary Lawrence Summers and former Council of Economic Advisers chair Jason Furman. Democratic lawmakers have been pressing the Fed to revive initiatives it launched to help smaller businesses and municipalities. For their part, Republican lawmakers have sought to limit the ability of the Fed to use nontraditional policy tools; in late 2020 they forced a phaseout of five emergency lending facilities, auguring further political battles, especially if asset price inflation continues. The administration of Joe Biden will have a chance to help shape the debate as he fills appointments on the Fed board.

There’s no doubt that massive monetary injections have made it easier for cash-strapped governments to fund budget deficits. They’re killing bond vigilantes, those investors who demand a greater return, especially for longer-dated securities, when a government’s borrowing soars to compensate for the added risk in being paid back. Nowadays central banks—explicitly in the case of Japan and Australia or implicitly in the case of the U.S. and some others—are damping even long-maturity yields with guidance that assures prolonged easy money.

Fed Chairman Powell alluded to the dynamic in a Dec. 16 press briefing when commenting on soaring U.S. stocks and their elevated price-to-earnings ratios. “Admittedly, PEs are high,” he said. “But that’s maybe not as relevant in a world where we think the 10-year Treasury is going to be lower than it’s been historically from a return perspective.” He spoke after the Fed linked its balance sheet expansion to achieving progress toward its inflation and employment goals—a marked evolution from the spring of 2020, when it was designed to avert a lockdown-induced credit squeeze.

For Paul Nolte, a portfolio manager at Kingsview Asset Management LLC in Chicago, Fed policy has been the key factor in his decision-making in the past year. When it became clear last spring that monetary policy was riding to the rescue, he says, it “was a moment of ‘aha, here comes the Fed.’ ” Starting in April, after monetary authorities began pumping liquidity into markets, he piled into high-yield bonds along with investment-grade credit and equities.

By the summertime, he found himself fielding calls from clients who were alarmed at his bullish market positioning, given mounting worries over a coronavirus resurgence. “Some of them called and said, ‘It’s too risky, we need to go to cash,’ ” Nolte says. “They couldn’t understand what kept the stock market going. I’d tell them, ‘The key to that is the Fed. You want to pay attention to the economy, but you need to pay even more attention to the Fed.’ ” Later in the year he was still favoring riskier assets, turning toward sectors including small-cap shares and emerging markets.

On the same day in December that Powell gave his stimulus assurance, Bitcoin breached $20,000 for the first time, en route to a 2020 gain of 305%. Scott Minerd of Guggenheim Investments told Bloomberg TV that the fair value of the world’s largest cryptocurrency still had a way to go. Its scarcity and “rampant money printing” by the Fed suggested Bitcoin would eventually climb to about $400,000, Minerd reckoned—though he tempered his enthusiasm in January, after Bitcoin slid as much as 21% over a couple of days, saying, “Bitcoin’s parabolic rise is unsustainable in the near term.”

While established crypto-traders remain the major force behind Bitcoin’s move, newcomers to the digital market including big companies and Wall Street investors are also a factor, says Hong Kong-based Bankman-Fried, who founded the derivatives exchange FTX and also heads the crypto-trading firm Alameda Research. “The low-yield environment is leading more companies to say, ‘Let’s put our money in Bitcoin,’ ” he says. “I am working 17, 18 hours a day and taking naps when I can in the office. All of our metrics are way up.”

Bubbles aren’t an economic problem until they pop. Efficient markets should price in the future, so rallying shares, house prices, bonds, and Bitcoin could all be signaling a robust expansion as the global economy shakes off the coronavirus shock. “The biggest risk is that the capital markets central banks don’t control start to misbehave,” says Michael Shaoul, chief executive officer at Marketfield Asset Management LLC. The medium-term pledge from central banks forswearing tightening, he says, “has already been priced into many financial decisions.”

One example: Private equity and other nonpublic investors have poured into commercial real estate even as the pandemic has raised questions about the future of cities. Despite its exposure to malls, restaurants, hotels, and offices that may face lower long-term revenue in a post-Covid world, commercial property has been rebounding. Premiums on U.S. BBB-rated commercial property bonds almost halved between May and the end of 2020, according to data Bloomberg compiled. That was despite delinquency rates on commercial mortgage-backed securities that as of November weren’t improving, according to Goldman Sachs Group Inc. For securities tied to lodging, the delinquency rate was almost 23%, and for retail it was 12%, according to a mid-December Goldman report.

With investors chasing returns wherever they can find them, the rising tide of money is flowing through to bonds sold by companies from poorer economies, too. This is the case even in nations that have been among the hardest hit by the pandemic. When AC Energy, part of Philippine conglomerate Ayala Corp., sold a $300 million perpetual green bond at 5.1% in November, CFO Dizon described the demand as “overwhelming.” Vaccine optimism, along with expectations for a strong recovery in 2021, helped clear the route for AC Energy’s fundraising. “In the morning we announced the mandate and in the evening we priced,” she says. “That usually takes two days. But we saw that the market was very strong, so our bankers recommended to just close everything in the day.”

For all the market optimism that abounded as the new year began, one thing was clear: The global economy will need a powerful recovery to justify lofty valuations in global stock markets.

In October, high-flying equities persuaded Einhorn’s Greenlight Capital to bet against what he called a “bubble basket of mostly second-tier companies and recent IPOs trading at remarkable valuations.” But to those who think that central bank stimulus is a solid foundation on which to make bets, Einhorn says the history of monetary policy in Japan and Europe shows that “artificially controlled long-term interest rates are no justification for stratospheric equity valuations.”

The surge in equities since the financial system’s darkest days in late March of last year—an advance that saw the S&P 500 index soar 68% from its low that month to the end of the year—also had companies rushing to take advantage of flattering valuations. Initial public offerings raised about $180 billion on U.S. exchanges in 2020, more than double the prior year’s total and far above the previous high of $102 billion set in 2000, according to data Bloomberg compiled. That included some blockbuster debuts, such as Airbnb Inc. more than doubling, up 113%, on its first day of trading, and DoorDash Inc. jumping 86%.

The IPO wave was also powered by a new investment structure involving so-called special-purpose acquisition companies that’s become increasingly popular in recent years. SPACs raise money through public offerings, using the funds to buy stakes in target companies they identify after they’re listed.

Until fairly recently, these companies focused on “value” sectors, where assets are perceived to be underpriced. Then came 2020. Not only did a record number of SPACs come to market, but 31% of them didn’t even specify an industry they were targeting, according to Goldman analysts led by David Kostin in a December report. Total proceeds more than quintupled. From the start of July through mid-December, the market averaged more than one SPAC IPO a day. “With the Fed committed to keeping the funds rates near zero, our view is that SPAC activity will continue at a high pace in 2021,” the report said.

Amid all the rippling effects—from central banks to government bonds to equities, real estate, and emerging markets—the most worrying dynamic for many is the explosion of new debt, both public and private. Borrowing grew $15 trillion in the first three quarters of 2020, to a record of more than $272 trillion, according to the Institute of International Finance. The Washington-based group warns that emerging-market debt, excluding banks, is quickly approaching 210% of gross domestic product, up from 185% in 2019 and 140% a decade ago. The fear is that falling revenues will make paying back that debt harder, even with low interest rates.

If inflation rises and central banks are forced to dial back on easing, then bond markets globally will feel the pain, perhaps even derailing any recovery. The Taper Tantrum of 2013 is illustrative. When then-Fed Chairman Ben Bernanke announced a future tapering of his quantitative easing program, U.S. Treasury yields shot higher, roiling markets around the world. This time around the exit ramp will be even more fraught with danger, given the larger scale of stimulus.

Even if things do work out as currently envisaged, there are risks. Japan is an example of the kinds of challenges that crop up if monetary policy remains stuck in place for a long time. Japanese investors have been effectively forced out of their country’s government bond market by the Bank of Japan’s voracious QE, destabilizing institutions that traditionally relied on parking investments in those securities, especially regional banks.

The Yoshihide Suga administration is working with the BOJ to rationalize the entire regional banking industry to head off potentially disruptive collapses in coming years. Other big investors, including the vast savings system run out of post offices, have turned to overseas investments, leaving them vulnerable if the yen appreciates and makes foreign assets worth less in domestic terms.

Another weakness highlighted by Japan’s generation-long experiment with ultra-easy monetary settings is that the quantitative easing has undermined longer-term productivity by propping up businesses that probably should’ve been allowed to fail. That’s what happens when governments and companies can borrow so cheaply that there’s no incentive to make structural fixes that inflict short-term pain such as job losses.

“Central banks [in advanced economies] are in a global liquidity trap,” says Jerome Jean Haegeli, chief economist at the Swiss Re Institute in Zurich. “The liquidity bazooka buys time and pushes up asset prices but has zero value in improving economic trend growth. Like a black hole, once you are in it, it is extremely difficult to get out. That’s where we are in central banking, we are in a liquidity black hole.”

The time for maximum bullishness—when policymakers are going all-out to jump-start their economies—may be coming to an end, leaving a trickier period looming on the horizon, says Richard Yetsenga, the chief economist of Melbourne-based Australia & New Zealand Banking Group Ltd. “While the risk profile for growth has been declining,” he says, “for asset prices and financial stability, it will soon be increasing.” —With Matthew Brockett, Katherine Burton, Elena Popina, Tassia Sipahutar, and Cecilia Yap

Anstey is a senior editor in Boston and Curran is chief Asia economics correspondent in Hong Kong.